Understanding Insurance: How to Safeguard Your Wealth and Tomorrow

Knowing about insurance is essential for anyone seeking to safeguard their monetary future. It provides a safety net against unexpected events which might result in major financial setbacks. A wide range of coverage options exists, each designed for different needs. Yet, numerous people find it difficult deciding on the appropriate level of protection and maneuvering through policy details. The complexities of insurance often lead to confusion, necessitating a better grasp on how best to protect one's wealth. What factors should people weigh before committing to a policy?

Fundamental Insurance Concepts: Key Principles

Coverage acts as a fiscal protective layer, protecting individuals and businesses against unexpected dangers. It is essentially an agreement linking the customer and the company, in which the policyholder remits a fee in exchange for financial coverage against specific losses or damages. The essence of insurance lies in risk management, letting policyholders pass on the weight of prospective fiscal harm to the company.

Insurance policies outline the terms and conditions, explaining which events are included, which situations are not covered, and how to report a loss. The idea of combining funds is key to insurance; numerous people contribute to the scheme, making it possible to finance payouts from those who experience losses. Grasping the core concepts and language is essential for making informed decisions. In sum, coverage aims to offer security, making certain that, when disaster strikes, people and companies are able to bounce back and continue to thrive.

Different Forms of Coverage: A Detailed Summary

Numerous forms of coverage are available to cater to the diverse needs of individuals and businesses. Among the most common are health insurance, that pays for healthcare costs; car coverage, guarding against damage to vehicles; and homeowners insurance, safeguarding property against hazards like burning and robbery. Term insurance grants fiscal safety to beneficiaries in the event of the policyholder's death, whereas income protection offers salary substitution if one becomes unable to work.

For businesses, liability insurance protects explore against claims of negligence, and property insurance covers physical assets. Professional indemnity insurance, often called E&O insurance, shields professionals against claims resulting from negligence in their duties. Additionally, travel insurance offers protection for surprises that occur during journeys. Every form of coverage is fundamental to risk management, helping people and companies to mitigate potential financial losses and maintain stability in uncertain circumstances.

Evaluating Your Coverage Requirements: Is Your Current Coverage Adequate?

Determining the appropriate level of insurance coverage requires a meticulous appraisal of the worth of assets and likely hazards. People need to evaluate their financial situation and the possessions they aim to cover to determine the necessary protection limit. Effective risk assessment strategies play a vital role in making sure that one is not insufficiently covered nor spending too much on superfluous insurance.

Determining Property Value

Evaluating asset value is an essential step in understanding how much coverage is necessary for sound insurance safeguarding. This process involves determining the worth of private possessions, property holdings, and financial assets. Those who own homes need to weigh factors such as current market conditions, replacement costs, and asset decline when appraising their property. Also, one must appraise physical items, automobiles, and any liability risks associated with their assets. Through creating a comprehensive list and appraisal, they may discover potential gaps in coverage. Furthermore, this assessment assists people customize their insurance plans to suit unique requirements, providing proper safeguarding against unforeseen events. In the end, correctly appraising asset value lays the foundation for sound insurance decisions and monetary stability.

Methods for Evaluating Risk

Gaining a comprehensive grasp of asset worth logically progresses to the following stage: determining necessary insurance. Methods for assessing risk include identifying potential risks and establishing the necessary amount of protection necessary to reduce those dangers. This process begins with a comprehensive list of possessions, including property, cars, and physical items, coupled with a review of possible debts. One should take into account elements like where they live, daily habits, and risks relevant to their profession that could impact their insurance requirements. Additionally, reviewing existing policies and finding coverage deficiencies is necessary. By quantifying risks and connecting them to the worth of assets, one can make informed decisions about the level and kind of coverage needed to protect their future successfully.

Grasping Policy Language: Key Concepts Explained

Knowing the policy provisions is vital for handling the complicated nature of insurance. Core ideas like coverage categories, insurance costs, deductibles, policy limits, and restrictions play significant roles in judging how well a policy works. A firm knowledge of these terms assists consumers in making sound judgments when selecting insurance options.

Explaining Coverage Categories

Insurance plans include a range of coverage categories, each designed to address specific risks and needs. Typical categories involve liability coverage, which shields from legal action; property coverage, safeguarding physical assets; and coverage for personal injury, which addresses injuries sustained by others on your property. Furthermore, extensive coverage offers protection against a wide range of risks, like natural catastrophes and stealing. Specific insurance types, like professional liability coverage for companies and medical coverage for people, further tailor protection. Understanding these types helps policyholders choose the right coverage based on their unique circumstances, ensuring adequate protection against possible monetary damages. Every coverage category is vital in a broad insurance approach, ultimately contributing to fiscal stability and tranquility.

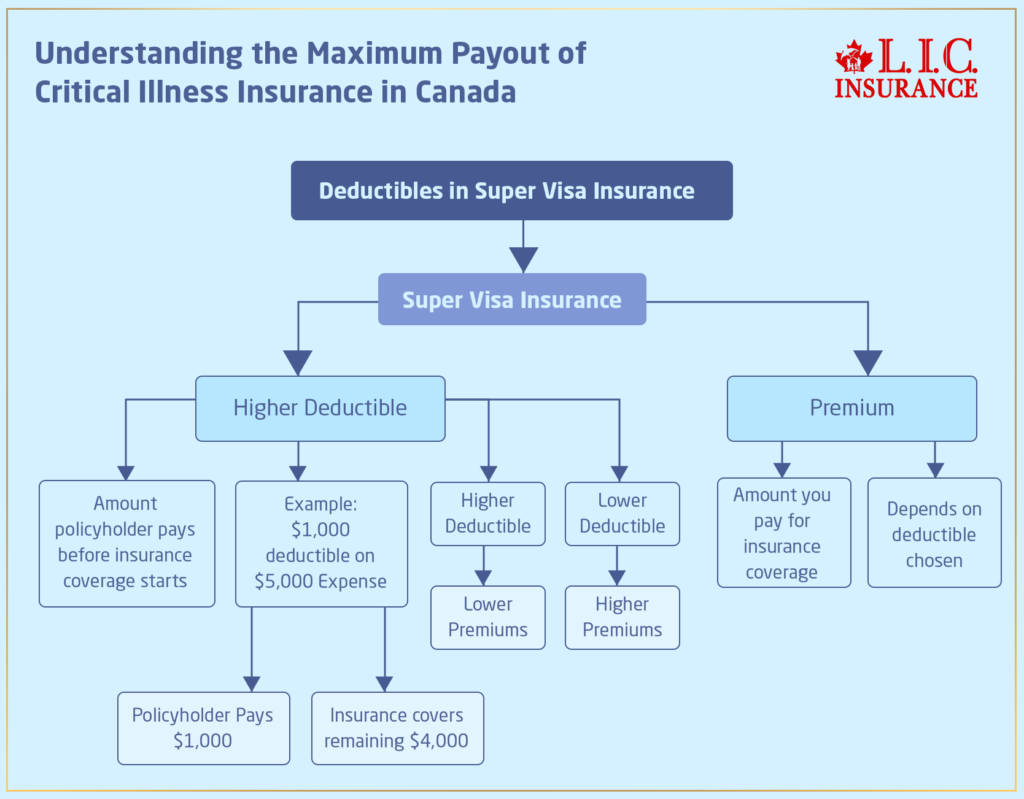

Insurance Costs and Out-of-Pocket Limits

Selecting the right coverage types is just one aspect of the insurance puzzle; the financial components of premiums and deductibles heavily affect policy selection. The premium is the fee for holding an insurance policy, typically paid monthly or annually. A greater premium often indicates more extensive coverage or reduced out-of-pocket costs. Conversely, deductibles are the amounts policyholders must pay out-of-pocket before their policy protection activates. Opting for a greater deductible can lower premium costs, but it could result in more fiscal liability during claims. Grasping the relationship between these two factors is essential for individuals seeking to safeguard their possessions while controlling their spending wisely. Crucially, the interplay of deductibles and premiums determines the overall value of an insurance policy.

Limitations and Exclusions

What elements that can reduce the utility of an insurance policy? Exclusions and limitations within a policy define the circumstances under which coverage is denied. Typical exclusions include pre-existing conditions, acts of war, and specific natural catastrophes. Limitations may also apply to maximum payout figures, necessitating that policyholders grasp these restrictions thoroughly. These elements can greatly influence payouts, as they specify what losses or damages will not be compensated. It is vital that policyholders examine their insurance contracts closely to find these restrictions, so they are well aware about the scope of their protection. Thorough knowledge of these terms is essential for protecting one's wealth and long-term financial stability.

The Claims Process: What to Expect When Filing

Filing a claim can often be confusing, especially for those unfamiliar with the process. The first stage typically requires informing the insurance company of the incident. This can generally be completed through a telephone call or online portal. When the claim is submitted, an adjuster may be appointed to evaluate the situation. This adjuster will review the details, collect required paperwork, and may even visit the site of the incident.

After the assessment, the insurer will determine the validity of the claim and the payout amount, based on the policy terms. Those filing should be prepared to offer supporting evidence, such as documentation or images, to help the review process. Communication is essential throughout this process; claimants may need to follow up with the insurer for updates. A clear grasp of the claims process helps policyholders navigate their responsibilities and rights, ensuring they receive the compensation they deserve in a reasonable timeframe.

Advice on Selecting the Right Insurance Provider

What is the best way to locate the ideal insurance provider for their needs? To begin, one must examine their unique necessities, looking at aspects such as the kind of coverage and budget constraints. Conducting thorough research is essential; online reviews, scores, and client feedback can provide information about customer satisfaction and service quality. Furthermore, obtaining quotes from multiple providers enables comparisons of premiums and policy details.

It's wise to check the economic strength and credibility of potential insurers, as this can impact their ability to fulfill claims. Speaking directly to representatives can clarify policy terms and conditions, guaranteeing openness. Furthermore, seeing if any price reductions apply or combined offerings can improve the total benefit. Finally, seeking recommendations from trusted friends or family may help uncover dependable choices. By taking these measures, people are able to choose wisely that align with their insurance needs and financial goals.

Remaining Current: Ensuring Your Policy Stays Relevant

After choosing a suitable insurer, policyholders should be attentive about their coverage to make certain it addresses their evolving needs. It is crucial to check policy specifics often, as major life events—such as tying the knot, home purchases, or professional transitions—can change necessary policy levels. Individuals should schedule annual check-ins with their insurance agents to talk about necessary changes based on these personal milestones.

Additionally, staying informed about industry trends and changes in insurance regulations can give helpful perspectives. This knowledge may reveal new coverage options or savings that could enhance their policies.

Monitoring the market for competitive rates may also lead to more cost-effective solutions without reducing coverage.

Commonly Asked Questions

How Are Insurance Rates Affected With Age and Location?

Insurance premiums typically increase with age due to increased risks associated with older individuals. Additionally, location impacts rates, as metropolitan regions tend to charge more due to more risk from crashes and stealing compared to non-urban locations.

Can I Change my insurance company Mid-Policy?

Yes, individuals can change their coverage provider mid-term, but they must review the terms of their existing coverage and ensure new protection is secured to avoid gaps in protection or associated charges.

What Happens if I Miss a scheduled premium?

When a policyholder skips a scheduled installment, their protection could cease, resulting in a possible lack of coverage. The coverage might be reinstated, but could require back payments and could include fines or higher rates.

Do pre-existing medical issues qualify for coverage in Health Insurance?

Pre-existing conditions may be covered in health insurance, but coverage varies by plan. A lot of companies require waiting periods or limitations, whereas some offer instant protection, emphasizing the importance of reviewing policy details thoroughly.

In what way do deductibles influence the cost of my coverage?

The deductible influences coverage expenses by determining the amount a policyholder must pay out-of-pocket prior to the insurance taking effect. Higher deductibles typically result in lower monthly premiums, while lower deductibles lead to higher premiums and potentially less out-of-pocket expense.